SBTi Net Zero Standard: Raising the bar

- Dec 3, 2025

- 3 min read

The Science Based Target Initiative (SBTi) has published the second draft of their revision to the Corporate Net Zero Standard. While it’s not final, it is in its latter stages. This is likely the last public consultation opportunity, which is crucial because this latest version raises the bar considerably. If you want to share your feedback, please do so by 12th December 2025.

Key changes in the Corporate SBTi Net Zero Standard

In terms of the proposed changes, several will significantly impact whether non-financial companies set and achieve an SBTi-aligned Net Zero target. Here are the most notable adjustments:

Expanded public disclosures. Public disclosures have expanded to include more specific and transparent information on target progress, mitigation measures, and plans to close gaps. Companies must consent to the SBTi publishing this information themselves. This likely indicates that a new or updated SBTi database is on the horizon.

Calculation of FLAG emissions. All companies must now calculate FLAG (forest, land, and agriculture) emissions. For many, these emissions will be minimal. For instance, an office-based service company may only need to consider paper purchases. However, this change means additional calculations and emission factors, which could incur costs.

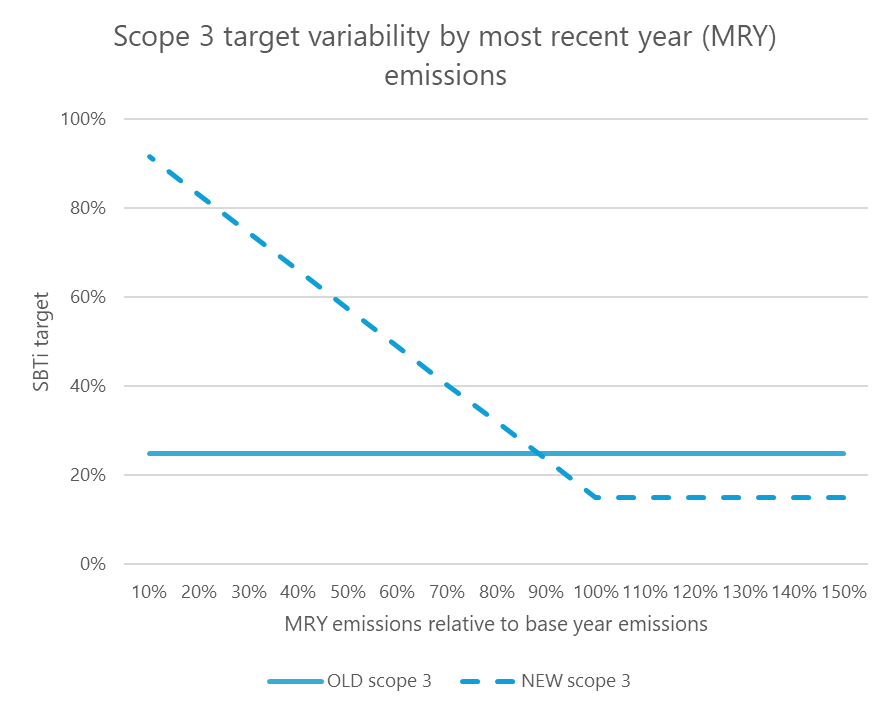

Base year requirements. A company’s base year must now be the most recent year of data. Previously, there was some flexibility, but that is no longer the case, except for extreme events like COVID-19. This change may make target achievement harder for some companies, as they can no longer benefit from historic reductions.

Separate targets for scope 1 and 2. Targets for scope 1 and 2 emissions must now be separate. With scope 2 generally being easier to reduce, this requirement will make target delivery more challenging for many companies.

Complexity in renewable energy use. The use of purchased renewable energy to achieve target reductions is now more complex. It seems to largely preclude the use of nuclear energy, as generation facilities must be commissioned or re-powered within the past ten years. Additionally, country and market matching could make achievement particularly difficult for companies operating outside the UK.

Additional requirements for Category A companies

For larger “Category A” companies, there are additional and much more demanding requirements. Currently, it’s challenging to identify which UK companies will fall into Category A because the thresholds are stated in both EUR and USD. For now, we will assume the lower of these two applies. The most impactful additional requirements include:

Transition plan publication. Companies must publish a transition plan within 12 months of target validation. I personally wouldn’t recommend setting science-based targets (SBTs) without a delivery plan. However, some specific requirements of the transition plan may make companies uncomfortable sharing them publicly, such as plan costs and financing approaches.

Additional metrics for validation. Additional metrics must be measured and disclosed during the validation process. While many of these metrics would be measured anyway, there are new requirements related to transport that could impose an additional data burden. For example, companies must report the percentage of light-duty vehicles that are electric, and emissions from scope 1 and 2 related travel must be reported as gCO2 per vehicle km.

Third-party assurance. Third-party assurance will be required for base year emissions, any recalculation, and data substantiating target performance. This requirement will not only add significant costs but will also extend the time needed for the pre-validation process.

Mandatory carbon removals. The purchase of carbon removals will likely become mandatory from 2035 for a defined percentage of emissions, with the value to be confirmed in the coming years. Current suggestions indicate this could be around 17%.

Complex scope 3 targets. Scope 3 targets are now more complex and granular. Instead of a single scope 3 target, multiple category-specific targets will need to be set. This includes individual targets for all supply chain commodities (categories 1 and 2) that represent more than 5% of scope 3 emissions.

Timing of the new standard

While companies can still set new targets under the current Corporate Net Zero Standard until December 2027, all companies will be encouraged to adopt the new standard starting January 2028.

Our perspective

What’s our take? We are passionate about companies doing their part to limit global warming. The SBTi currently lacks effective mechanisms for checking progress post-target setting, so we support these changes. However, the increased bureaucracy surrounding transition planning, reporting, and assurance, along with the future requirement to invest in carbon removals, will significantly raise costs for larger companies. This might deter them from setting targets altogether. If that happens, the influence on the supply chain to set targets diminishes, and ultimately, the environment could suffer.

We believe a less rigorous and scientifically perfect approach that is actually implemented is likely to be better than a comprehensive solution that never sees the light of day.

If you want to share your views with us or discuss the impact on your targets, contact us.

Authored by Caroline Johnstone.